As a quick refresher, you can claim CPP between the ages of 60 and 70. If you take it before 65, the amount you receive is reduced. If you take it later, it is increased.

The Break-Even Approach

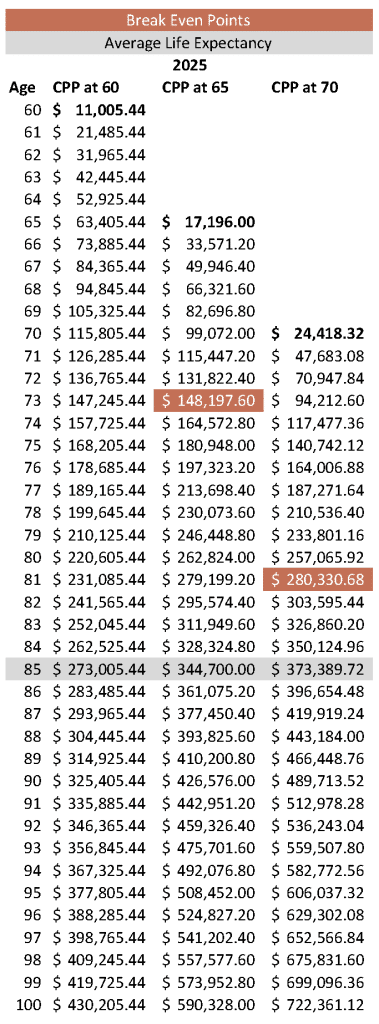

Most people have heard of the break-even approach, which shows how long it takes for the cumulative amount received from delaying CPP to catch up to what you would have received if you took it earlier. Here is an example using the maximum amount from 2025.

*This table is for illustration purposes only.

You can see that waiting until 65 pays off at age 73 because, by then, you will have received more money overall. Similarly, waiting until 70 pays off at age 81.

While this information is helpful, the problem with this approach is that we obviously don’t know how long you’ll live, and it is isolated – it does not consider your entire financial picture or what you value most.

How Much Does It Matter?

Of course it matters, but the decision about when to take CPP will be more critical to some than others.

Regardless of any of these points, if you really need the money, start taking the benefits. If you are terminally ill, start taking the benefits. Whether or not you need it is the first determining factor; everything else follows.

If it feels like you need it but aren’t sure what your options are, consider talking to a professional to help you review your financial picture.

Beyond that, if you run the risk of running out of money during your lifetime, the decision about CPP deserves closer attention. If you have ample retirement savings and that risk is lower, your decision becomes more guided by preferences and values.

There are some important caveats, which we will get into in the Tax Impacts + Government Benefits section.

Key Preferences and Values to Consider

Outside of real need and the known variables, there are some key preferences and values to consider:

1. Life Expectancy

Deciding when to take CPP is challenging primarily because none of us know how long we have. While there are life expectancy calculators and life tables, the best we can do is make an educated guess. Without this key variable, it is hard to calculate the option that gives you the most spending power over your lifetime.

To build off our previous point, if you’re confident you’ll die sooner, you may consider taking CPP sooner. Otherwise, understanding the average 60-year-old will live until 85 can be helpful.

Together with the break-even approach, you can see that delaying CPP can make sense. However, other considerations can change this.

2. Tax Impacts + Government Benefits

Both very low-income and higher-income people have specific considerations.

*If you consider a dollar of benefit (whether it be CPP, OAS, or GIS) not received the same as a dollar in tax paid, this section will matter more to you.

- If you expect your retirement income to be very low, you may qualify for the Guaranteed Income Supplement (GIS). In this case, it is important to consider that CPP is included in your income for this calculation. If you are confident you would qualify for GIS with a lower CPP payment, you may consider taking CPP earlier to improve your chance of qualifying for GIS and increasing your overall government retirement benefits.

- If you expect your retirement income to exceed the OAS clawback amount (now called the OAS pension recovery tax), meaning your OAS will begin to be clawed back, you may consider taking CPP early. However, above a certain income – roughly $150,000 in 2024 – this strategy does not apply anymore.

Your whole financial picture matters in both examples.

Additional Tax Impacts:

- Receiving CPP and OAS increases your taxable income, which affects eligibility for programs like Pharmacare. The Medical Expenses Tax Credit is also reduced based on income. If you start receiving benefits early, the payments will be smaller, so the impact on your taxable income will be smaller.

I wouldn’t weigh the ‘Additional Tax Impacts’ too heavily. Here, you are trying to determine which scenario gives you the best net benefit, and sometimes, decreasing CPP to increase a different tax advantage will not benefit you overall. It depends on your specific circumstances.

3. Fixed Income vs. Inheritances

This is where your values and overall financial picture become more important.

CPP is similar to certain pensions in that when you die, your spouse may receive a reduced pension for the rest of their lifetime. However, children or other family members would receive next to nothing. There is a $2,500 CPP death benefit, and that’s it.

If your retirement income includes a combination of CPP and personal retirement savings, and you are trying to decide whether to delay CPP and start depleting your retirement savings or take CPP at 65 and delay depleting your savings, this section may prove helpful.

Fixed-Income Focus:

If one of your highest priorities is the security of a larger fixed pension-like income for a lifetime, you may choose to spend your retirement savings first and delay CPP. However, this can come at the cost of leaving an inheritance.

It’s important to note that, like some pensions, a spouse can expect a CPP Survivors Benefit for the rest of their life, though it will be a reduced amount.

Inheritance Focus:

If your inheritance wishes extend to children or others, you might choose to take CPP earlier, around 65, to optimize your spending and your ability to leave an inheritance. Remember, even if you have not spent all the CPP contributions you made throughout your life, you do not get a lump sum at death. You get $2,500, no matter how soon or late it happens.

If you have loved ones you value more than other Canadians in general, you may choose not to delay CPP past 65. If you spend most of your retirement savings and pass away early, the CPP income you would have received goes back into the CPP fund for others. If instead you choose to preserve your retirement savings and spend CPP earlier, like at 65, there would likely be more left for your loved ones after you pass on.

Important Note: If your priority is increasing your spending power over your lifetime, delaying CPP still may not be the best way to do this. If your retirement savings are invested in equities, you may still be able to increase your lifetime spending power by taking CPP around 65 and allowing your investments to grow as you spend a differently weighted combination of the two.

This can get a bit complex, so I recommend engaging with a professional to discuss if you’re interested.

4. Inflation + Rate of Return

I am combining these two considerations because they impact each other.

CPP is adjusted for inflation, so if your external retirement savings do not have a rate of return that matches or exceeds inflation (averaging around 3% per year), you may be better off delaying CPP, because your savings will be eroding in a way that your CPP income is not.

However, if your rate of return on investments is higher than inflation and the combination of the rate of return and the size of your retirement investments exceed the benefit of delaying CPP, you may be better off taking CPP around 65.

Important Note: It is often a misnomer that you can create more spending power by taking your CPP at 60 and investing it. Especially if you do not have sizable investments, the impacts often break even too late, depending on the size of your investment portfolio.

Conclusion

All in all, there is no blanket solution or obvious answer about when to take your CPP. Because we do not know how long we will live, it is largely left to your preferences and values. You can make this decision for yourself or engage with a professional to make a decision that feels right for you.

Let’s work together

Book Appointment